| Fundamentals of Statistics contains material of various lectures and courses of H. Lohninger on statistics, data analysis and chemometrics......click here for more. |

|

Home  Basic Concepts Signals and Data Types of Noise Basic Concepts Signals and Data Types of Noise |

|

| See also: signal and noise, physical origin of noise, Scedasticity |   |

Types of NoiseNoise can be classified into several categories. For the description

of noise, one can use three statistical properties which are described

in more detail below.

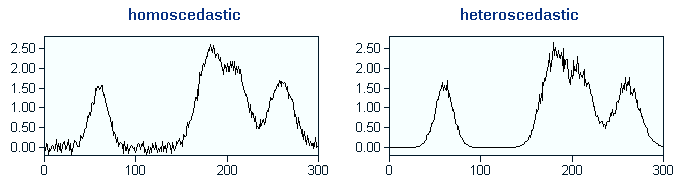

StationarityWhen the characteristics of a random process do not vary over time, the process is called stationary. A generalization of stationarity is ergodicity. A random process is ergodic when its properties are the same for different samples. Of course, only stationary processes can be ergodic. Ergodic processes are an important class of processes, since their properties can be determined from a single sample.The properties of a non-stationary process vary over time. One special aspect of non-stationary processes is the changing of the variance in the process. When the variance of the random process is constant, we speak of homoscedastic noise. Its opposite is called heteroscedastic noise, i.e. the variance changes with the height of the signal (often it is simply proportional to it).

In order to get more information on homo- and heteroscedasticity, please

start the following interactive example .

AutocorrelationUsually we assume that the random errors are completely independent of each other. The error at one specific time does not influence the error at another time. This is the assumption of independence. However, in practical signals we often find that this assumption is not true and the random parts of the signal are (auto)correlated. We speak of autocorrelation because the correlation occurs within the same signal. The degree of correlation between random errors at different times can be described by the autocorrelation function (ACF) or its equivalent, the power spectral density (PSD). Engineers have given the different shapes of the PSD the names of colors:

DistributionIn most cases the noise exhibits a normal distribution. Complex instruments have many sources of noise that are convolved with each other, resulting in a normal distribution due to the central limit theorem. But in certain instruments one process is predominant and it determines the type of the distribution. When we count electrons or other particles at a low rate, the noise is Poisson distributed. When the noise follows a well-known distribution, it can be described by a set of parameters. |

|

| Home Basic Concepts Signals and Data Types of Noise |

|